The SpaceX IPO (Ticker: SPCX) is currently at the absolute peak of its pre-market climax. It is slated to be the largest initial public offering in global financial history—dwarfing Saudi Aramco’s 2019 record ($29.4 billion) by aiming to raise a staggering $75 billion at an implied valuation of roughly $1.75 to $1.8 trillion.

The shares are priced at $135 each, and the official public trading debut on the Nasdaq is scheduled for tomorrow morning, Friday, June 12, 2026.

Here is the breakdown of where things stand right now and the tactical engineering behind the massive play for retail investors.

1. The Latest Status: Massive Oversubscription

The order books officially closed for institutional buyers ahead of tonight’s final pricing, and the numbers are unprecedented:

- 3.5x to 4x Oversubscribed: Total investor demand across all tiers has blown past $250 billion.

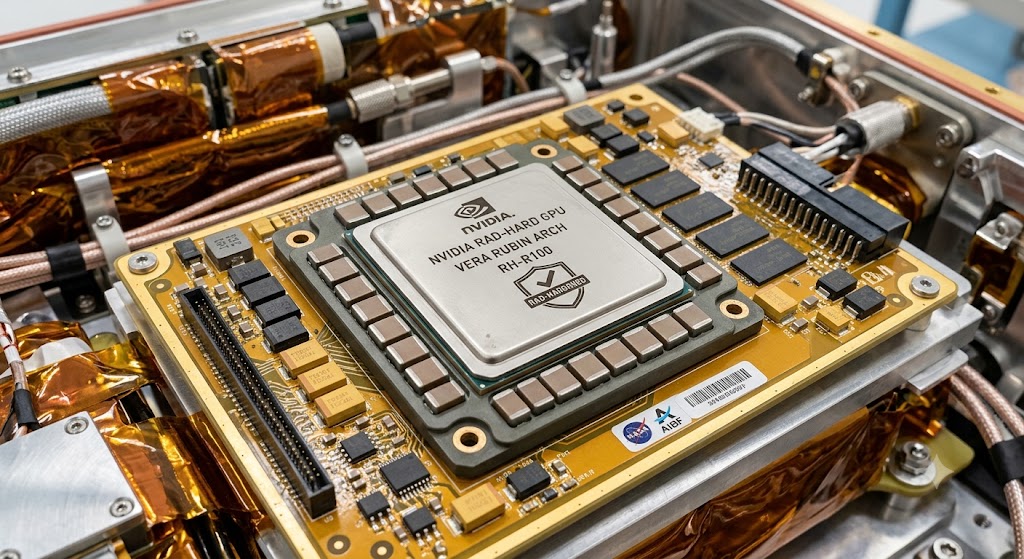

- The Valuation Driver: While Starlink’s satellite broadband dominance remains the primary revenue driver, leadership heavily pumped the valuation narrative this week by unveiling “AI1”—SpaceX’s upcoming 230-foot space-based AI data center satellite built on the Starlink V3 bus using Nvidia hardware.

- The S-1 Financial Reveal: The public prospectus showed that while the growth story is massive, SpaceX lost roughly $5 billion last year, heavily compounded by its recent structural merger with xAI.

2. Why Leadership is Over-Allocating to Retail Investors

Typically, a mega-cap IPO reserves a tiny sliver—about 5% to 10%—of its shares for everyday retail investors, leaving the rest to sovereign wealth funds and massive asset managers. SpaceX is completely flipping this playbook, intentionally allocating an unprecedented 20% to 30% of the entire $75 billion offering strictly to retail buyers via platforms like Robinhood and Charles Schwab. Retail demand alone has reportedly crossed $100 billion.

Leadership is aggressively courting the retail market for three distinct strategic reasons:

A. Diluting Institutional Governance and Maintaining Absolute Control

Elon Musk currently commands roughly 85% of shareholder voting power at SpaceX. In a standard IPO architecture, flooding the gate with multi-billion-dollar institutional allocations (like the Middle Eastern sovereign wealth funds currently bidding) creates large blockholders who can demand board seats, push for strict financial transparency, and challenge volatile, capital-intensive long-term goals (like Mars infrastructure).

The Strategy: 100 million individual retail investors holding 20 shares each cannot organize a proxy vote or challenge corporate governance. By fracturing up to 30% of the float into tiny, uncoordinated retail hands, current leadership effectively silences a massive chunk of the public float, ensuring unchecked operational control.

B. Creating a “Floor” Against the Post-IPO Slump

Historically, massive tech IPOs suffer severe volatility or deep “drawdowns” 6 to 12 months after going public as institutions cash out. Retail investors—particularly those fiercely loyal to Musk’s brand ecosystem—behave completely differently.

- As seen with Tesla (TSLA), retail investors tend to “HODL” (hold on for dear life), buying the dips based on ideological belief in the mission rather than rigid quarterly EBITDA metrics.

- By backing the IPO with a baseline of highly passionate, less price-sensitive individual investors, SpaceX creates an artificial buffer against aggressive institutional short-selling.

C. Gaining Leverage over Index Trackers

Because of the sheer size of SpaceX ($1.8 trillion), index providers (like S&P and Nasdaq) are actively overhauling their “seasoning” rules to fast-track SPCX into major benchmark indices far faster than the typical months-long waiting period. However, index inclusion requires a healthy, liquid public float. Securing massive retail participation guarantees massive, highly active day-one trading volume. This liquidity profile forces passive index funds to aggressively buy up the remaining institutional shares post-debut to properly mirror their benchmarks, driving a powerful mechanical “pop” in the stock price.

If history is any indicator, when the broader market finally does the math and realizes that the foundational infrastructure—whether it’s the Mars colonization timelines, heavy Starship infrastructure, or the newly minted “AI1” orbital data center constellations—is an 8-to-10-year engineering trudge rather than a next-quarter revenue driver, the stock price faces a very predictable, multi-stage mechanical correction.

Morningstar’s valuation model published today perfectly frames this reality. They calculated the “fair value” of SpaceX’s current functional business (Starlink broadband and Falcon 9 cargo delivery) at around $63 per share. At the $135 IPO price, investors are paying a $72 per share “option premium” purely on faith in future moonshots.

When the market starts pricing out that premium, here is exactly how it plays out across the timeline:

Stage 1: The “Honeymoon” and Technical Squeeze (Months 1–3)

Even if institutional analysts write scathing notes about execution delays, the price will likely remain artificially insulated or even push upward early on.

- Passive Buying Floods the Gates: Because of its historic $1.75+ trillion size, major index providers are fast-tracking SPCX into global benchmarks. Index-tracking funds are legally forced to buy hundreds of millions of shares regardless of timeline realities.

- The Retail HODL Effect: The massive 30% allocation to retail acts as a fundamental shock absorber. Retail investors who bought into the ideological “multi-planetary” mission don’t trade on traditional discounted cash flow (DCF) models; they hold through bad news, keeping supply tight.

Stage 2: The S-1 Reality Check & Margin Compression (Months 6–12)

The real price pressure begins when the first few quarterly earnings reports drop.

- The “CapEx” Reality Shock: Investors will see billions of dollars in capital expenditure (CapEx) burning through the balance sheet with zero immediate yield. As the capital requirements for Starship infrastructure and xAI integration compound, the $75 billion raised in the IPO will look less like a war chest and more like a temporary runway.

- The Valuation Multiples Compress: Growth stocks are valued on a multiple of future earnings. When a timeline stretches from 2 years to 8 years, analysts must apply a heavy discount rate to those future cash flows. A longer timeline means money is tied up longer under higher risk, which mathematically forces the current target share price down.

Stage 3: The Lock-up Expiration Wave (Month 6)

This is the structural danger zone for the stock price. Over 4,400 current and former SpaceX employees are about to become overnight paper millionaires. When the standard 180-day insider lock-up period expires, a massive wave of supply hits the market. Early employees looking to diversify, buy homes, or lock in life-changing wealth will sell, creating a severe structural headwind that retail buyers alone cannot absorb.

The Ultimate Price Trajectory: The “Amazon Playbook”

If the infrastructure takes 8 years to catch up, SPCX will likely follow the classic Gartner Hype Cycle curve, mirroring Amazon’s trajectory from 1999 to 2007:

The Drop: Once the initial excitement fades and the reality of a decade-long infrastructure build sets in, the stock will likely bleed out its speculative option premium, correcting backward toward its fundamental valuation baseline (closer to that $63–$80 range) where it is valued strictly as a satellite telecom and defense contractor.

The Consolidated Accumulation: It will trade sideways for years in a painful, volatile consolidation pattern. Institutional money will treat it as a “show me” stock, refusing to bid it back up until tangible technical milestones (like fully autonomous orbital refueling or certified space-hardened GPU clusters) are actively proven.

The Payoff: The investors who survive that grueling multi-year plateau are the ones who get rewarded if and when the infrastructure finally goes live, converting the speculative option into a literal monopoly over orbital infrastructure.